Student Loans, Consumer Credit and the Hungry Beast

Is consumer debt dragging us down?

When I am out in the real world and I have the chance to opine about the state of consumer spending, a question I often get after such opining is, “what about credit cards or student loans? Doesn’t consumer debt matter?”1

The answer, of course, is “yes,” consumer debt matters. In aggregate, we have piled up a lot of debt. At the end of June of this year, the total amount of consumer credit totaled about $4.6 trillion, and that number doesn’t include mortgage loans. The issue, too, is currently making headlines, with the Biden Administration announcing plans to forgive student loans for certain borrowers.

But, from a macroeconomic perspective, the current state of consumer debt—and its potential drag on consumer spending—may not be as dire as the popular imagination might assume. At least, the situation may not warrant the ubiquitous portents of doom seen in the popular press.

So, let’s check out some data to see what the “state of consumer” debt looks like.

Student Loans

The data we will focus on is aggregate student loans, as tallied and reported by the Federal Reserve (in the “G.19” data release, available here and here).2 The series is available since 2006, shown below in current dollars and in percent change.

The top panel of the figure shows what many already know, student loan debt has steadily increased. And, the amount is substantial—increasing from $521 billion in 2006 to $1.7 trillion in 2021. While this series only goes back to 2006 (the earliest date the data is available in the G.19 release), it is easy to imagine this series has only increased since such loan programs existed.

One sliver of a silver lining is shown in the bottom panel of the figure. The year-to-year increase in the debt has declined over the same period, from a high of 13% in 2006 to under three percent in 2021. What has driven this decline? I do not know and, at least for this post, I’m not going to speculate (the post is already on its way to being long enough).

So, for student loans, the total is a lot and has increased year after year. But, at least the growth rate has slowed down substantially.

Now let’s examine all consumer loans.

Consumer Lending

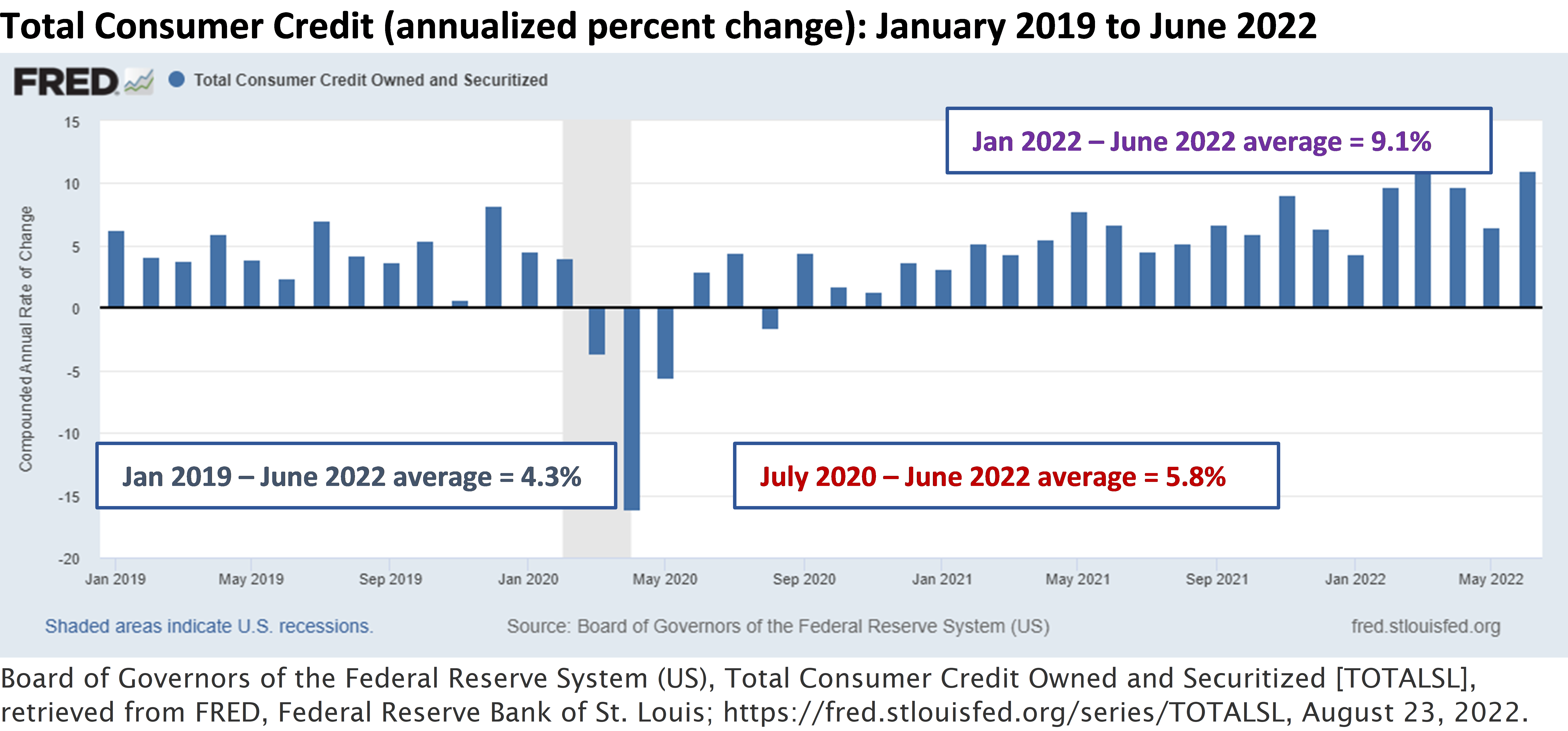

The Federal Reserve G.19 release focuses on consumer credit. The headline statistic is “total consumer credit,” which includes car loans, credit card loans and personal consumer loans (and excludes mortgage loans or, “loans secured by real estate”). The total also includes the students loans that we focused on just above. The figure below shows month-to-month changes of total consumer credit owned and securitized since January of 2019.3

As noted on the figure above, the average annualized change of outstanding consumer credit is 4.3 percent since January of 2019. Since we came out of the “Covid-19 Recession,” the average change is 5.8 percent, while the average for the first six months of 2022 equals 9.1 percent. In the most recent month recorded, June, the rate equaled 11.0 percent.

How do these “trends” compare to history? If we go back to 2000, the January 2000 to June 2022 average equals 5.2 percent. (Those years are not shown on the graph; I calculated that average after downloading the data.) With that perspective, the 2019 to June 2022 average or the July 2020 to June 2022 average shown on the chart are not that far off the “long-term” average. However, the average for 2022 thus far certainly is!

How should we interpret the boost in consumer credit for 2022? One could interpret the increase in consumer loans outstanding as evidence consumers are struggling to maintain consumption spending—using credit cards, specifically, to keep up with inflation (as many news articles suggest). Alternatively, one could interpret the increase as evidence that consumers in the aggregate are not that concerned about the broader macro picture—they are spending regardless.

In fact, historically, consumer credit tends to be pro-cyclical—increasing as the economy expands, and decreasing as the economy contracts. For example, during the Great Recession—spanning December 2007 through July 2009—consumer credit averaged a negative 0.1 rate of change (I calculated these stats from the aforementioned downloaded data). During the Great Recession, consumer credit increased for only the first few months—from December 2007 to July 2008—but the increases over those months got smaller and smaller. Starting in August of 2008, consumer credit growth was negative for 9 of the remaining 11 months of the Great Recession. The average over that span was a negative 2.8 percent.

Of course, previous business cycles are illustrative, not proof of what will happen next time. While consumer credit is not declining now, that does not mean consumers won’t throw up their collective hands and slam the brakes on spending (and credit card spending) over the second half of 2022.

One more chart

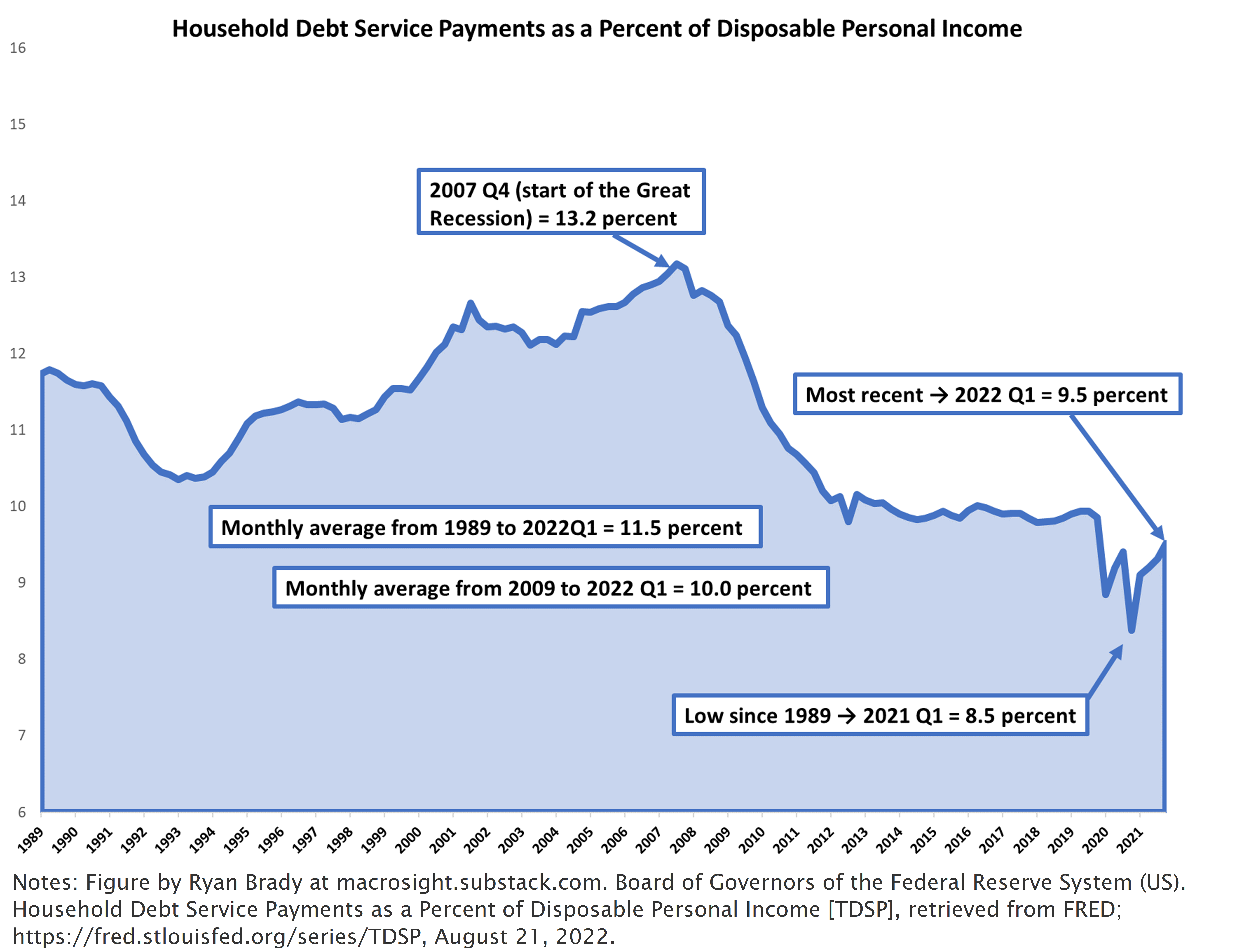

A popular statistic related to consumer debt is “Household Debt Service Payments as a Percent of Disposable Personal Income.” The numerator of the statistic is a combination of mortgage payments and payments on consumer loans (see the notes at this link for detail; the series is available here or here ).

The figure below shows this statistic back to 1989 (you can see the series back to 1980 at either of the just-mentioned links).

As annotated on the figure, the historical peak of this statistic was the very end of 2007, which was the start of the “Great Recession” (as dated by the NBER). Since that peak the value has declined. The most recent data point is for the first quarter of this year, equaling 9.5 percent—which is close to the average that prevailed from 2009 through 2019. The historical low for the statistic occurred in the first quarter of 2021. The sharp drop in that quarter, and the drop in early 2020, are both associated with boosts to disposable income (as can be seen here).

So, if part of the concern about consumer debt is that consumers are on the precipice of a financial meltdown, this statistic does not suggest that, at least not as of yet. Our “debt burden” is below levels that existed during the 1990s and up to and including the Great Recession years. That is not to say—just like in the case of consumer credit discussed earlier—that things can’t change. But for now, the aggregate view of consumer credit, and student loans, implies that consumers en masse, by historical comparison, are not in disastrous financial shape.

In full disclosure, I have embellished this opening anecdote. Outside of the classroom, I have had only one conversation with a non-economist related to consumer spending—at least that I can remember—and that covers about 20 years of a personal macroeconomic-studying experience. In a social setting, talking about economic data is a good way to never be invited back to said setting. However, on that one occasion a person really did ask me about consumer debt.

From notes to the G.19 Release: “The Student Loans memo item reflects the total student loan debt outstanding, including accrued interest and defaulted federal loans. The estimate is constructed by summing private (non-guaranteed) student loans and federal student loans outstanding issued under the Direct Loan, the Federal Family Education Loan, and the Perkins programs.”

The data goes back decades, but for the sake of focus and relative brevity, I show the data back to 2019.