The Anatomy of the Business Cycle

GDP growth over the Short Run vs the Long Run

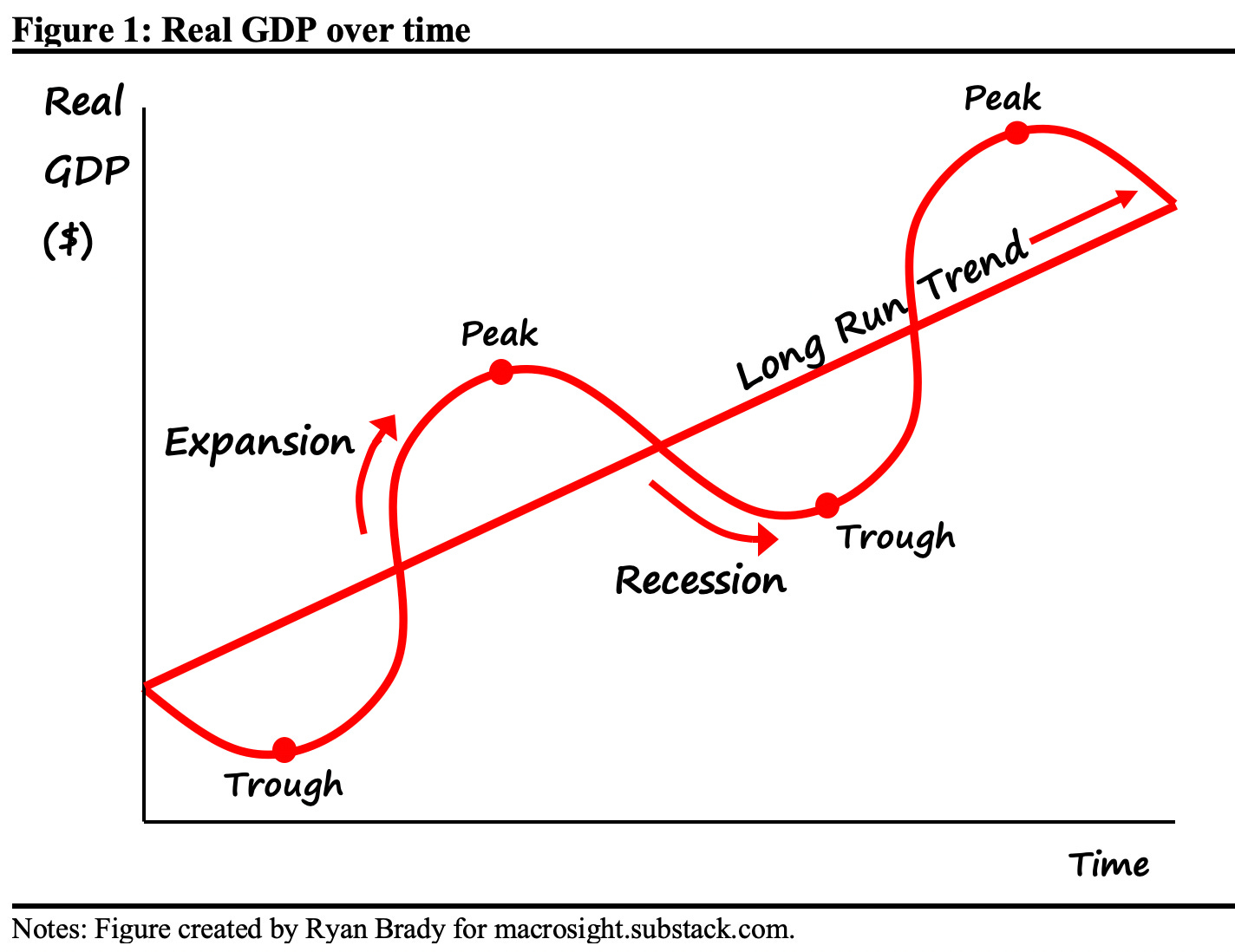

When I teach macroeconomics, I like to draw this picture on the white board:

This picture, showing the increases and decreases in the dollar value of real GDP around a trend, emphasizes the dual nature of the macroeconomy. One part, the trend, reveals the fact that when we look back over decades, we can see our economy has grown consistently. The other part, the increases and decreases around that trend reveal that, consistent growth aside, it has been an up and down ride. This ride is otherwise known as the business cycle.

In the study of macroeconomics, we call the business cycle the “short run” and the trend line the “long run.” The juxtaposition between the long run and the short run guides our understanding of not only the macroeconomy itself, but also macroeconomic policy. Stabilization policy, for example, is primarily about the short run. Let’s consider the short run and the long run in turn, starting with the long run trend.

The Long Run

The “long run” is both a hindsight view and a projection forward. With respect to the former, notice that in my simple picture above, the trend line shows the dollar value of real GDP goes up and up in a perfect linear fashion (implying a constant growth rate). Yet in hindsight, it is clear that the actual path of the economy over time is not exactly straight. From 1950 through 1984, for example, average real GDP growth equaled 3.5 percent. From 1985 through 2019, growth slowed to an average of 2.5 percent.

If we drew trend lines separately over those time periods, the trend line would be steeper for the former and flatter for the latter. If we focused in on shorter periods, we would see more sub-periods of faster or slower growth. And, if we looked even closer we would see yet more frequent ups and downs, i.e., the business cycle.

Hence, the long run trend emerges when we zoom out. If we look back over a long period of time from, say, 1950 through 2023, the trend line that emerges splits the difference of the different growth rates across decades, and all the cycles in between. Imagine using a ruler to find the middle of the cycle shown in Figure 1, but doing so over 70 years’ worth of data. That is the gist of fitting the trend line.

In that respect, the trend line provides a “hey, look how far we’ve come” perspective. However, what is also important about the trend line is that it provides the best guess of where we are going. When we look to the future and extrapolate the trend we call this “potential GDP.”1

What is funny about the long run, however, is that trend line is formed in real-time, day-by-day, month-by-month and year-by-year. Splitting the difference of the business cycle does not mean that those ups and downs around the trend do not matter, or all wash out in the end. On the contrary, the magnitude and duration of those ups and downs have an impact on the future path of GDP, making our estimate of Potential GDP very uncertain and dependent on the short run.

The Short Run

The business cycle is characterized by two broad phases, “expansions” and “recessions.” There is no exact definition of each, so let’s use the visual in Figure 1 to see how most economists characterize these phases.

To sharpen the definitions above, notice on the left-side of Figure 1 the first point marked “trough.” The trough is the lowest point of a particular cycle (identifying the farthest point below trend). Once we are past that point, economic activity increases from period-to-period (and the growth rate of real GDP is positive). As we move along the cycle beyond the trough, we continue to expand past the trend-line until we hit the peak. This part of the cycle, from trough to peak, is the “expansion” phase of the business cycle.

Once we are beyond the peak, economic activity contracts period-to-period and does so until we hit another trough (along the way the growth rate of real GDP will be negative). From peak to trough is the recession phase of the cycle. Then we do it all over again.

Figure 1, of course, makes the cycle look like a nice predictable sine way. In reality, the business cycle is irregular and an expansion or a recession in one decade is going to look different than an expansion or a recession in another decade, with different peaks, troughs, and duration of time to move from one to the other.2

Consider, for example, a comparison of the 1990s expansion and the early-2000s expansion. The 1990s expansion lasted 39 quarters from the second quarter of 1991 through 2000.3 Real GDP growth averaged 3.7 percent and the rate of unemployment fell from 6.7 to 3.9 percent. The next expansion, from the first quarter of 2002 through the third quarter of 2007, lasted 23 quarters and growth averaged 2.9 percent. The unemployment went from 5.7 to 4.7 percent.

Similarly, every recession is different. The 2001 recession lasted four quarters, over which GDP growth averaged a positive 2.5 percent, while the unemployment rate went from 4.2 to 5.7 percent over the course of the year. The Great Recession, in contrast, lasted seven quarters, with GDP growth averaging -1.8 percent. Yet, that average understates the severity of that recession, which had successive quarters of -2.1 percent, -8.8 percent, -4.5 percent, and -0.7 percent, the latter of which marked the trough in the second quarter of 2009. The unemployment rate went from 5.0 percent at the end of 2007 to 9.5 percent by the second quarter of 2009.

Looking back over history, from 1945 to 2020, expansions as dated by the NBER have lasted an average of about five years (64 months or 21 quarters), while recessions have lasted an average of less than a year (just over three quarters or about 10 months). We have been fortunate in that regard, and this fact of our business cycle helps us understand why the long run trend line has marched up and up, instead of flat-lining or even declining over stretches of time. Our long expansions have allowed us to recover from the setbacks and losses suffered during a recession. Yet, that is not meant to imply that even as the trend has persisted upwards, somehow recessions have not mattered, or do not matter.

Economic Pain

It is difficult to say exactly how any particular recession has altered the path of our long run growth. But we can try. To do so, let’s look at how much the Great Recession cost us in terms of lost output.

Figure 2 displays quarterly real GDP (billions of 2017 constant dollars) from 2006 through 2012.

The bars shaded grey mark the quarters of the Great Recession which ran from the fourth quarter of 2007 through the second quarter of 2009.4 Real GDP actually reached a historical peak in the early part of the recession, but as one can see that did not last for long. By the second quarter of 2009—the trough—real GDP had contracted by almost $700 billion.

While the trough technically “ends” the recession, notice the slow climb back up from that trough. It took real GDP another six quarters to get back to where we had been in early 2008. That implies that almost three years’ worth of economic progress had, in a sense, been wiped off the books. As if we froze in place in early 2008, only to thaw out more than 10 quarters later to find ourselves standing in the same place.

While the U.S. economy continued to march upward after 2010, and even survived Covid-19, it is easy to imagine how the Great Recession, and that long-slow climb back to where we had been before, forever altered what could have been. Instead of Potential GDP springboarding upwards from that peak in 2008, our future trend-line was irrecovably stunted by those three years of loss and slow recovery.

Unemployment Coda

The unemployment rate at the end of December 2007 equaled 5.0 percent. Only seven months prior it had been as low as 4.4 percent. By October of 2009, the unemployment rate reached a high of 10 percent. At the end of 2010—the point at which real GDP had “re-gained” what was lost—the unemployment rate still stood above 9 percent. It wasn’t until September of 2015—2015!—that the unemployment once again was as low as 5 percent.

Over a period of eight years, millions of people lost their jobs and then waited, and waited, and waited to get back to work (the number of employed persons fell by about 9 million from January of 2008 to February of 2010, the nadir of the decline). Some lost their jobs and never returned to the labor force. At some point most did. But in the interim they lost months of income, perhaps years’ worth for many; they lost out on contributions to their retirement funds; to investments in their own long-run plans, to their family’s long-run plans; and otherwise had to restart their lives in some way. And when they did they more than likely faced a lifetime of lower salary and benefits than what they had expected from their careers prior to the Great Recession. Aside from that it is well-documented that recessions and the associated job loss are accompanied by increases in divorce, suicide, drug and alcohol abuse.

The loss of real GDP discussed above, in other words, is a sanitized representation of the economic—and social destruction—that can occur during a recession. Indeed, the personal loss that recessions bring underscore the motivation of the Fed—charged with carrying out stabilization policy—to maintain our economic expansions as long as possible.

The dates associated with past recessions and expansions, as determined by the National Bureau of Economic Research’s “Business Cycle Dating Committee,” are defined exactly thus, peak to trough for the former and trough to peak for the latter (see here). To choose when those turning points occurred, the committee considers a number of factors (see here for details), and they do so, typically, well after the fact since the troughs and the peaks are only obvious in hindsight. Any reference to specific recession or expansion dates in this post are based on the NBER-determined dates.

The NBER dates the business cycle at the monthly frequency but also provides a quarterly version; here we are using the quarterly version.

Technically the Great Recession began in December of 2007, but given the quarterly data we start the beginning with the fourth quarter of 2007.