The Natural Rate of Unemployment

The unemployment situation and the chance of a recession

Last week Jerome Powell and Co. boosted their interest rate target by 50 basis points (a half of a percent). It is the first time they have raised their target rate by that amount since the year 2000 (as noted in this article). While this was a bit lower than my subconscious was hoping for, it is a step in the right direction in the Fed’s now-urgent attempt to squash inflation. Powell also gave a press conference where he affirmed the Fed’s responsibility for bringing inflation down (as summarized succinctly here). That was nice to hear.

As far is this Fed watcher is concerned, I view these latest developments optimistically. And, on the heels of the previous post on the current, and historic, unemployment rate, I’d say there is a decent chance that Powell and the FOMC can pull of a “soft-landing.” Exactly what are the chances of a soft-landing? I’d say the chances are at least 50 percent. That is, there is a better-than-a-coin-flip-chance that they will be able to bring inflation down without tipping the economy into a recession. At worst, I’d put my money on a “mild recession.”

I realize that “at least 50 percent” is not very definitive. I’d say, however, it’s as good of a “forecast” as any. Any number you read in the financial press that is more precise—78 percent chance of a recession, 44 percent chance, etc.—is not necessarily backed by precise analysis. There are a lot of assumptions that go into any forecasting model. Whichever method the prognosticator used—whether that be a statistical model or not—at best it’s an educated guess. Though, I should add that I am not necessarily criticizing the people providing those estimates; forecasting models provide just that, educated guesses.1 And if I was getting paid to provide such estimates, I’d probably make them sound more precise, too. But I digress.

Why am I optimistic? Because of our current historic unemployment rate and how that rate compares to the “natural” rate of unemployment.

The Natural Rate of Unemployment

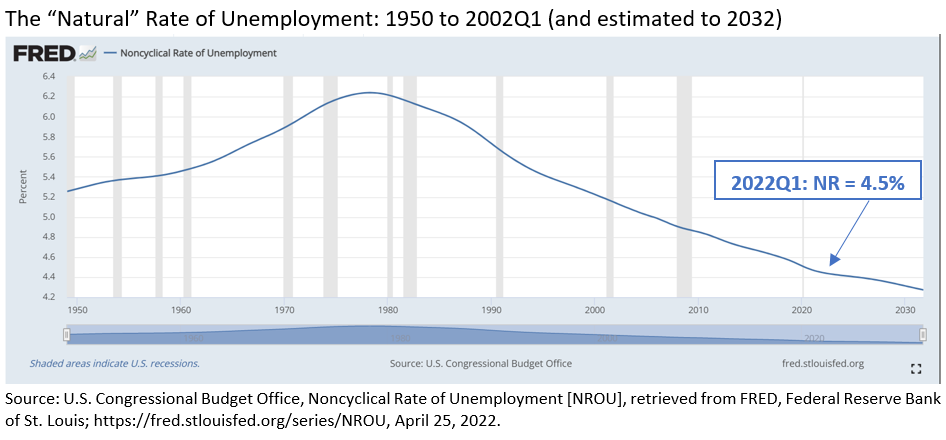

In textbooks the “natural rate of unemployment” is defined (generally) as the “normal” rate of unemployment around which the actual, in real-time, unemployment rate revolves. Another way of saying that is the natural rate is the rate of unemployment that exists when the economy is at Potential GDP. It represents a “healthy” level of unemployment for the macroeconomy where everyone that wants a job has one, and (ideally) a job that they want and for which they are well-suited. Like the Congressional Budget Office (CBO) do for Potential GDP, they also provide an estimate for the natural rate, though the concept is now referred to as the “non-cyclical” rate of (long-term) unemployment. The CBO defines this as follows:

“The noncyclical rate of unemployment (NAIRU) is the rate of unemployment arising from all sources except fluctuations in aggregate demand.”

As suggested in the name, the CBO relabeled the concept as the “noncyclical rate.” However, you are still likely to see it as the “natural rate” in most textbooks. In this post that is what I will call it.

The natural rate since 1950, as estimated by the CBO, is as follows:

The key thing to notice is that the noncyclical (natural) rate has changed over time. It peaked in the 1970s at just over 6.2 percent, fell below 6.0 percent by the early 1990s and has kept falling thereafter. The estimated natural rate for the first quarter of this year is 4.5 percent, while the CBO forecasts the rate will fall to 4.27 by end of 2032.

The so-called natural rate changes because the economy changes and the labor force changes. For example, if it takes people longer to find a job on average (say, right after college or after being laid off from a down-sizing industry), the natural rate will be higher. That is just one example; there is a lot more to it, the detail of which is too much for just one blog post. For more on the details check out this article from the NBER, or if pressed for time, you can get a succinct explanation from this video.

For our purposes—to guesstimate on the possibility that the Fed can hike rates without causing a recession—the important thing about the natural rate is to compare it to the actual unemployment rate.

The figure below shows just that.

In this figure I focus on the period just prior to the Great Recession to our current state of existence. The red line is the natural rate and the blue line is the actual unemployment rate (for the latter, you can see the entire series here, or you can check out my previous post on the subject). As the picture reveals, the unemployment rate was well above the natural rate during the Great Recession (as would be expected), and also for a long time after. Only in late 2016/early 2017 did the unemployment fall below the natural rate. Currently, too, the unemployment rate is below the natural rate and has been for about six months.

If we zoom in on more recent history we can see that more clearly:

What does it mean?

The gap in the picture above, where the unemployment is well below the natural “long-run” rate, is part of the reason myself and others have pointed out that the macroeconomy has been very strong (e.g. as exemplified by real GDP growth). For me, looking at the gap—among all the other evidence—makes it a no-brainer to say the economy has been, and still is, unusually strong.

However, for that reason, too, I suspect the Fed has some “room” to work with. From the vantage point of stabilization policy, the Fed can fight inflation, as is clearly needs to do, without putting the economy on a path to a “deep recession.” The Fed’s interest rate hikes are very likely to help push the unemployment rate up. Yet, given the gap in the picture above, it is reasonable to guesstimate that an unemployment rate increase to about 4.5 would be consistent with stabilizing inflation without “serious” damage to real GDP growth. In other words, there needn’t be a recession for them to accomplish the task before them. The gap suggests it is possible the Fed could pull this off.

Of course, my “analysis” here is conceptual. Based on the concept of stabilization policy, we can compare the current state of the unemployment rate to the “natural rate.” From that set up, we can then speculate on the possibility of a recession in a “thought experiment” kind of way. That is what I have done here. To go beyond a simple “thought experiment,” we obviously need to dig deeper. One way to do that is to look at the empirical history of the relationship between the unemployment rate, the Fed’s interest rate target, and real GDP (not necessarily in that order). Indeed, I will do just that in future posts.

One last thing: please note that saying there “needn’t be a recession” does not imply some sort of “rosy” picture. In that scenario there will be an economic slowdown and people will lose their jobs. Perhaps the best way to couch this scenario—avoiding a “deep” recession and getting mild recession, or near-recession instead—is that things will be less miserable than they otherwise could be. And, saying that the Fed can “pull this off” is faint praise, at best.

While it is rare to read details about the methods a pundit has used to come up with a forecast, that doesn’t mean they are hiding something. If said pundit tried to provide some description, no doubt the listener/reader would be put to sleep by such detail.