The very-low-Unemployment Rate and Fed Rate Hikes

“A Recession is Coming” . . . But what kind?

In Xanadu did Kubla Khan

A stately pleasure dome-decree:

Where Alph, the sacred river, ran

Through caverns measureless to man

Down to a sunless sea.

I had a dream recently that the Fed surprised everyone with an 80-basis point interest rate hike. And by “dream” I mean that literally. In that dream the Fed held a surprise meeting—in between its regularly scheduled meetings—and dropped the 0.80 percent increase on markets first thing in the morning. In the dream, I learned about the unexpected rate hike as I walked into my forecasting class. Then I woke up.

There is plenty of chatter with respect to the Fed’s forthcoming series of rate raises, with a number of headlines pointing to the impending doom of a “deep recession” or the stock market feeling the effects of a slowing economy. Not all are that pessimistic, however. The economists at Goldman Sachs are a little more optimistic, predicting real GDP growth to be 3.1% in 2022 with the unemployment rate falling to 3.3 percent by the end of the year (as reported in this YahooFinance article).1 As the article on Goldman’s estimates points out, the 3.1 percent growth rate of real GDP would be the second highest annual growth rate for our economy in 17 years (the first being last year’s historical number).

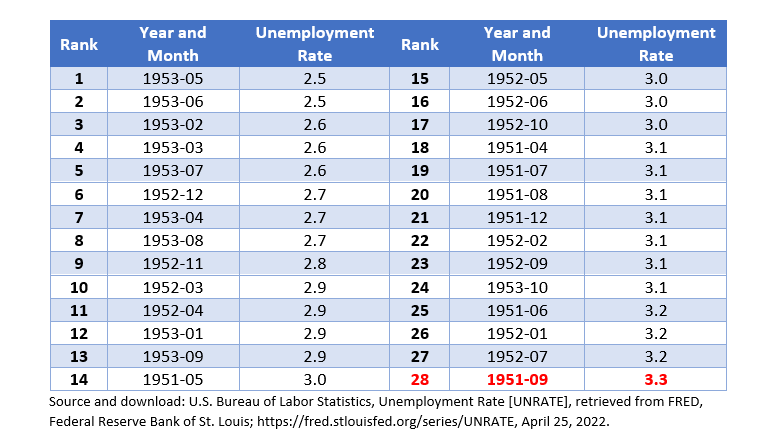

What the article does not state, however, is that a 3.3 percent unemployment rate, measured at the monthly frequency, would be the lowest the U.S. economy has experienced since September of 1959. 1959!!

The Historical Context

Here is a snapshot of the times we have had an unemployment rate at 3.3 percent or lower (since 1948):

We have not seen an unemployment rate of 3.3 percent or lower since the early ‘50s. For a different visual perspective, here is the entire series at the annual frequency (with the annual rate for 2021 (3.9 percent) highlighted along with the previous annual lows that were anywhere close to Goldman’s 3.3 percent estimate):2

Or, here are all the years the annual unemployment rate has been 5.0 percent or lower:

The unemployment rate for 2021 was tenth best since 1948. The rates for 2018 and 2019 are also in the top ten of lowest annual rates. If Goldman’s forecast bears out, a rate of 3.3 percent would supplant 1968 as the third best annual unemployment rate since 1948.

Given this information, let’s ponder a bit what the historical record of unemployment rate implies about the Fed’s planned rate hikes, and the possibility of a forthcoming recession (as a result of those hikes).

Mild Recession or Deep Recession?

Unfortunately, my dream did not last long enough for me to see what happened to the unemployment rate after the Fed’s surprise 80 basis point hike—so I can’t be like Samuel Coleridge and lay out the prediction from my dream. However, using the historical record, we can speculate. Will we have a “deep recession”? Or, will the picture be rosier, as the one forecasted by Goldman Sachs?

First, recall the typical textbook definition of a recession: real GDP growth is negative for at least six months. By that definition, for the Fed to cause a recession the interest rate increases they impose need to, at a minimum, lead to a negative growth rate of GDP for at least two quarters.

However, many economists take a broader view of a recession. Yes, we should expect negative growth as part of that recession, but we also need to consider the unemployment rate (among many other variables). So, let’s say we have a GDP growth rate around zero or just below zero, with an unemployment rate approaching about six percent. Let’s call that a “mild recession.”

For example, we had a mild recession in 2001. Real GDP growth was negative in the first and third quarters of that year (with growth rates of -1.3 and -1.6, respectively). The unemployment rate at the monthly frequency peaked at 5.7 in December of 2001. Interestingly, the unemployment later went above 6.0 percent in mid-2003, but technically the recession lasted from March 2001 through November 2001.3

Of course, mild or not, as can see in the figure shown earlier in this post, with the grey shaded regions showing the NBER-dated recessions, the unemployment rate always rises in a recession (see footnote 3 for more on the NBER). Sometimes the increase is dramatic, other times less so, like the case of the 2001 recession.

With that in mind, what should we expect if a “deep” recession occurs? The best example of a deep recession, in my opinion, is the Great Recession. The Great Recession is dated by the NBER from December of 2007 through June of 2009. The unemployment rate increased from 5.0 percent in December of 2007 to a peak of 10.0 percent in October of 2009. The unemployment rate also stayed elevated for a long time after, not failing back to 5.0 percent until September of 2015.

With that perspective, I think a reasonable definition of a “deep” recession is one where the unemployment rate shoots well above 6 percent and approaches 10 percent (or beyond, of course). For a mild recession, I think it reasonable to put that range between 5 and 6’ish percent. These are rough approximations, of course. Every recession is different, and past recessions do not necessarily predict the characteristics of a future one. But, we can at least take a look at history, and establish those parameters, in order to set our expectations for what’s coming. With that context, we might ask:

Or,

What are the chances the unemployment rate will approach 10 percent sometime over the next two years—that we end up in a deep recession?

Or,

What are the chances the unemployment increases to 5 or 6 percent and real GDP growth is low but still positive? In other words, we have a mild recession?

Our historical experience helps put those questions into better perspective. Personally, I suspect Goldman’s “rosy” forecast is a bit optimistic. However, given the very low unemployment rate we currently have, I would be surprised if we saw the unemployment rate above 5 percent by the end of this year. Admittedly, however, this is just conjecture, based on a simple reading of the historical record.

What next?

In addition to the historical context, we need to understand a lot more about the unemployment rate, among other aspects of our current situation. For example, we need to consider,

How does the current unemployment rate compare to the “natural rate of unemployment”?

How is the unemployment rate affected by people who drop out of the labor force (like many folks appeared to have done the past 18 months or so)?

How have interest rate increases affected real GDP and the unemployment rate in the past?

Or, is the economy already in a nose dive because of all the other things going on?

This post is already long enough, so we will take up those issues in future posts.

For a refresher on the definition of the unemployment rate, this is from the BLS: “The unemployment rate represents the number of unemployed as a percentage of the labor force. Labor force data are restricted to people 16 years of age and older, who currently reside in 1 of the 50 states or the District of Columbia, who do not reside in institutions (e.g., penal and mental facilities, homes for the aged), and who are not on active duty in the Armed Forces.”

The annual frequency here is defined as the rate at the end of the year. In the article about Goldman’s predictions, they cite the rate for 2021 as 3.9 percent, which is the rate at the end of 2021. Hence, I stick with that definition. I also considered the annual rate as the average of the monthly rates for the year. While the numbers then vary slightly, the general inference I make in this post is effectively the same regardless of the annual definition.

“Dating” a recession is not an exact science. In fact, by tradition the “official” dates of recessions are determined by a group of economists at the “National Bureau of Economic Research.” There is no legal mandate for them do so; yet, this source is more or less considered the de facto official designator of recessions. You can read how they determine recession dates here.