The Fed stands pat

Two reasons why Jerome Powell & Co. did not lower rates

This past week the Fed left its target interest rate at 5.25 percent.1 This decision came out of the first 2024 meeting of the policy making group known as the “Federal Open Market Committee,” (or FOMC, for short). This decision, too, disappointed many. To rub salt in those wounds of disappointment, Jerome Powell down-played the chances of any cuts in the very near future.

Why was anyone expecting rate cuts? In their last meeting of 2023, the Fed’s forecasts revealed that Powell and the FOMC anticipate lowering their target rate by about 80 basis points (or 0.8 percent) over the course of 2024. Figure 1 displays a snapshot of that forecast.

The FOMC has seven scheduled meetings remaining in 2024, suggesting that at least at a few of those meetings the rate will be cut.2 Hence, it has been reasonable for anyone to expect that the target interest rate will come down in 2024.

But, why was anyone expecting rate cuts now, one month into 2024?

I don’t know.

They shouldn’t have.

And here are two reasons why.

Reason 1

Real GDP growth is still “too high,” as discussed by Macrosight recently. The current estimate of real GDP growth for the fourth quarter of 2023 equals 3.3 percent. Given that estimate and the values for the first three quarters of 2023, the annual growth rate of real GDP in 2023 currently stands at about 2.5 percent. While those numbers may not make your eyes pop out, what is important is how those numbers compare to the Fed’s forecast for 2024 and its long run estimate for real GDP growth—which currently stands at only 1.8 percent. How do I know that? Because they told us so in their forecasts.

First, the Fed forecasts that real GDP growth will slow to 1.4 percent in 2024. Any rate cuts to get the interest rate to 4.6 percent are entirely dependent on that coming to fruition.

Second, the long run estimate of 1.8 percent represents something extremely important when it comes to understanding stabilization policy (explained here by Macrosight). That value represents the “baseline” growth rate for our macroeconomy at which the rate of inflation is “stable” around the Fed’s target inflation rate (2 percent) and the unemployment rate is close to the “noncyclical rate of unemployment” (explained here by Macrosight).

Simply put, GDP growth, especially the 3.3 percent reading from last quarter, is still well above that baseline. That implies the Fed cannot yet assume the rate of inflation will continue to fall, even though it has the past few months. Such strong growth relative to the baseline implies that inflationary pressures have not yet ebbed to the point of comfort for the members of the FOMC.

Reason 2

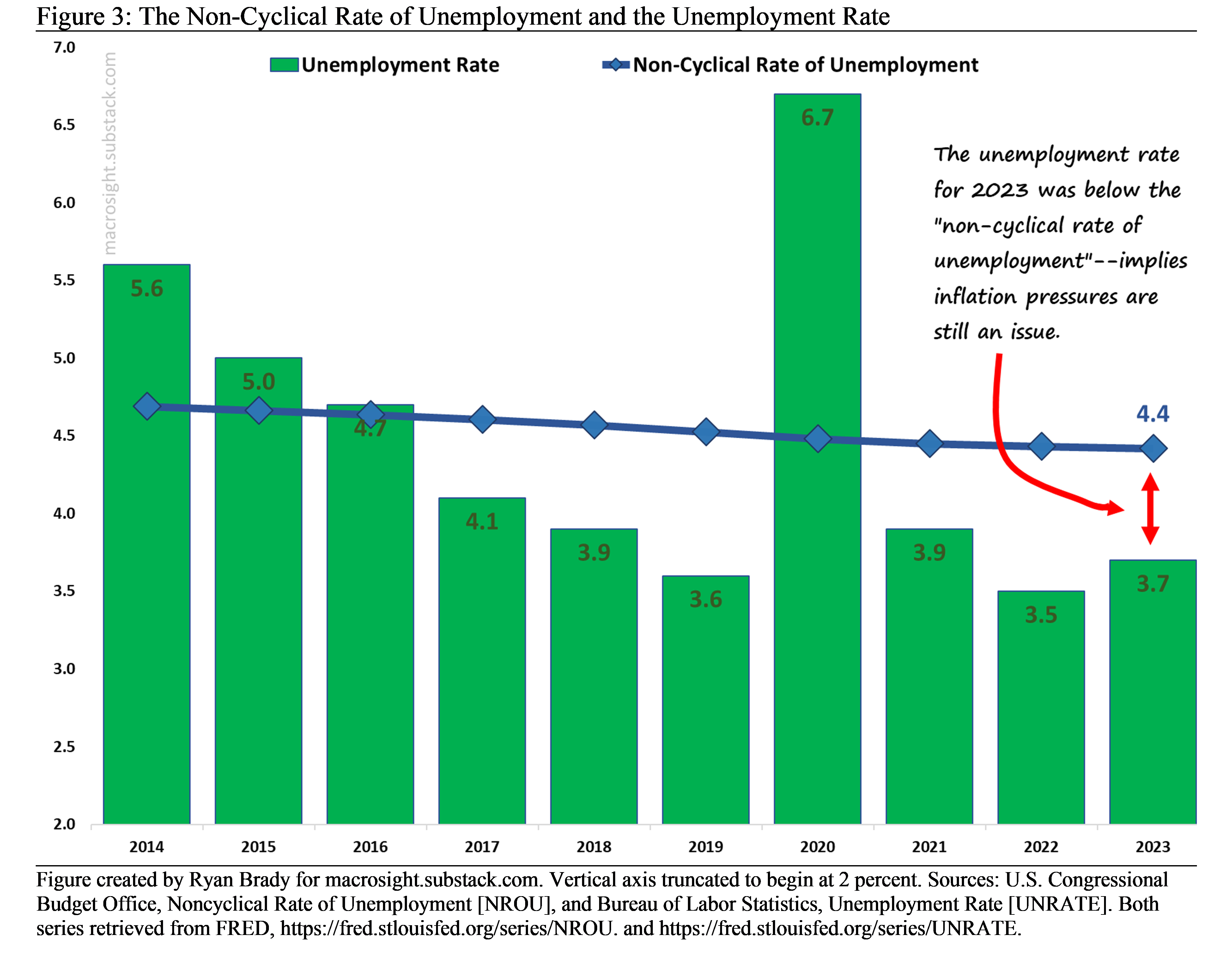

Consistent with the relatively “high” recent real GDP growth rate, the unemployment rate remains historically low and, as such, is below the noncyclical rate of unemployment. Figure 3 provides a snapshot of the annual unemployment rate over the past decade juxtaposed against the noncyclical rate of unemployment.

In the media, one might see this state of affairs described as a “tight labor market.” In the Fed’s press release from their December meeting they described—in a manner befitting the monotonal macroeconomics professor you remember from college—the labor market as thus: “Job gains have moderated since earlier in the year but remain strong, and the unemployment rate has remained low. Inflation has eased over the past year but remains elevated.”

Regardless of how one articulates the point, when the unemployment rate < non-cyclical rate, inflationary “pressures” remain a specter of which to be wary.

Also, just today, the Bureau of Labor Statistics (BLS) released the unemployment rate for January of 2024. That number is 3.7 percent, suggesting the labor market is showing no signs of rising back towards the non-cyclical rate of 4.4 percent, at least not yet. The same jobs report shows that the number of jobs added in January is much higher than was expected, providing further validation for the Fed’s cautious approach.

Be Patient, Not Surprised

For those two reasons, all macroeconomic and Fed-watchers should remain patient. Real GDP growth remains relatively high, and the unemployment rate remains relatively low. Those two facts are reason enough for the Fed to have stood pat this last week. And as long as those two facts continue to describe our macroeconomy, don’t bet on rate cuts anytime soon.

Technically the Fed specifies a range, which is currently 5.25 to 5.5. Due to market forces in the daily federal funds rate will fall somewhere in this range.

Why a few meetings? Because the FOMC will likely drop the rate target in 25 basis point increments, instead of an all-at-once cut of 80 basis points.