The Fed's Rate-Hike Surprise Non-Surprise

How a 4.4 % interest rate matters for 2023 GDP.

This past Wednesday the Federal Reserve’s monetary policy committee once again raised their interest rate target by about 75 basis points. Not surprisingly, the stock market took a dive upon hearing that news.

What is funny about that dive, however, is that the Fed’s policy move should not have come as a surprise. The Fed told us back in September that such a hike was coming. In fact, they told us that two such hikes were/are coming before the end of 2022. How did they tell us? They put that information in their forecast, published immediately after their September meeting. You can see that on their website, or from this partial screenshot of that forecast here:

Notice that the “projected path” for the Federal Funds rate for 2022 is 4.4 percent. The day that forecast was published, the federal funds rate was raised to (about) 3.0 percent. Hence, the Fed was telling us there was another 1.4 percent worth of raises to go!

With the rate now standing about 3.7 to 3.8 percent, that leaves another 75 basis points for the December 13-14 meeting.1 Barring terrible inflation readings in October and November, it seems a pretty good bet that in December the Fed is going to follow through with their plan and push the rate up to 4.4 (“terrible” would probably be any inflation number north of 7 percent).

That prospect begs the question: what will such a rate hike do to GDP in 2023? I touched on that question at the end of my post on GDP a couple weeks back, so let me finally answer it.

The rate-hike baseline forecast

It is logical to assume that an increase in interest rates will have an effect on spending. As rates increase, borrowing become more expensive and there is an incentive to save more and spend less. Expenditure across the economy should decline, all else equal.

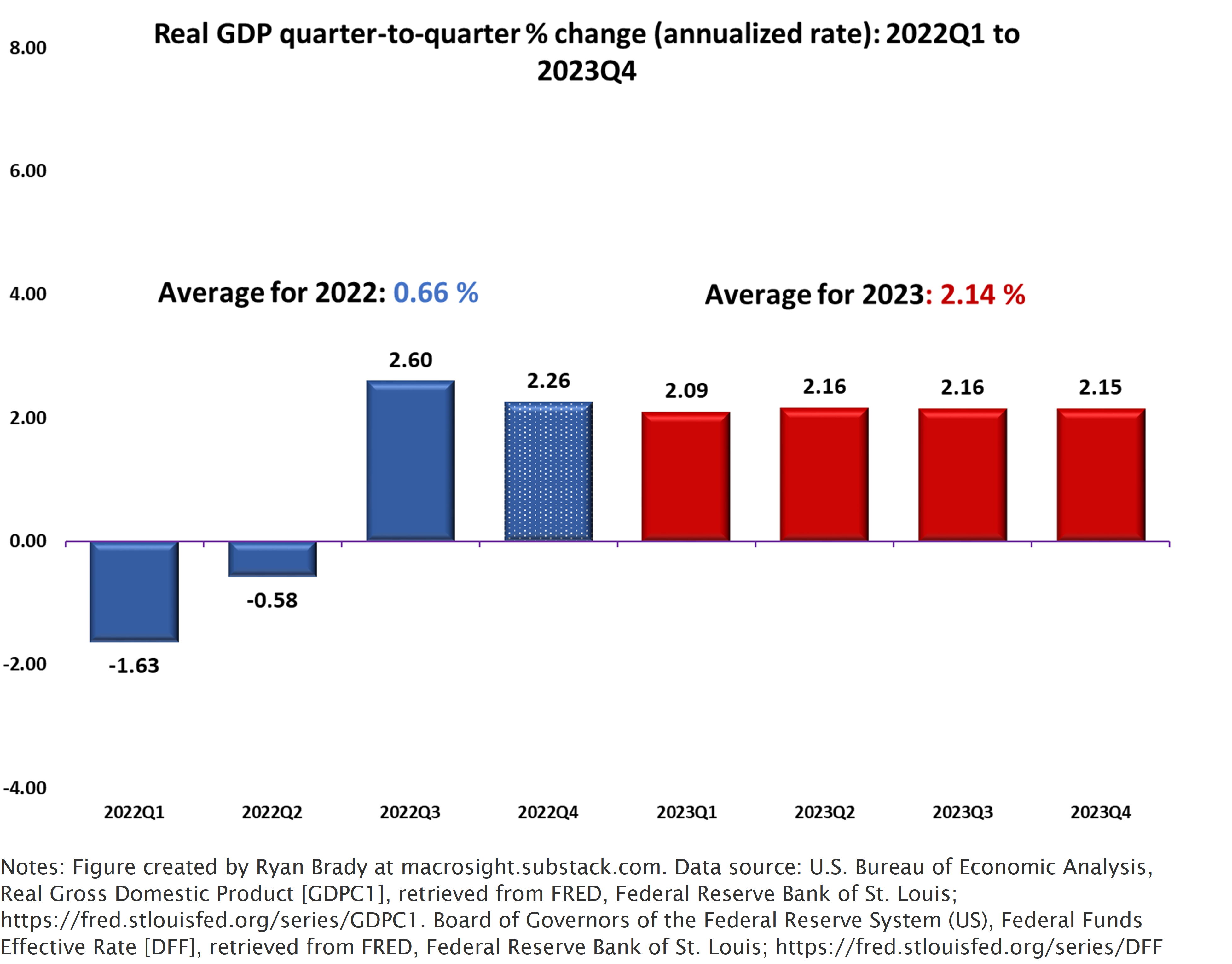

To see by how much, I tweaked my forecast for GDP to get a sense of how the Fed’s policy changes will matter for GDP in 2023. In my last post, I provided a forecast prior to the BEA releasing their estimate of 3rd-quarter GDP. That initial estimate is now in (2.6 percent). Given that knowledge, my baseline forecast for real GDP over the next five quarters is as follows:

By baseline, I mean that the model is estimated with only the last two quarters of real GDP growth used as inputs (as I explained in this post). That is, the baseline forecast does not include the federal funds rate as an input. From this baseline model, my forecast for average GDP growth is 0.66 and 2.14 percent in 2022 and 2023, respectively. Both values are more optimistic than the Fed’s latest forecast for real GDP (0.2 and 1.2 percent for 2022 and 2023, respectively).

To assess the impact of the Fed’s rate hikes on real GDP, I included the federal funds rate as an additional input in my model. I also made assumptions on how strong the effect of a change in the interest rate is on real GDP. I considered three values, –0.25, –0.5, and then, –1.0.

An “effect” of –0.25 means the following: as the interest rate increases by 1.0 percent (or 100 basis points), real GDP growth falls by 0.25 percent (25 basis points). Or for a value of –1.0, for every increase in the rate of 1.0 percent, real GDP growth falls by 1.0 percent. This latter assumption is likely extreme, but I include it as a “worst” case effect.2

I call these three escalating scenarios, my “soft-landing” forecast, my “turbulent” forecast, and my “brace-for-impact” forecast.

The “soft-landing” forecast

If I assume an effect of –0.25, my forecast is as follows:

My forecast estimates from the “soft landing” model are much closer to the Fed’s. It is certainly the case that the Fed is factoring the federal funds rate into their forecasts. Hence, it makes sense that by doing so in my model, I get closer to their values.

The “It’s-getting-turbulent” forecast

If I bump up the effect of a change in the interest rate on GDP to –0.5, the forecast is now,

Not surprisingly, if you assume a stronger effect of the interest rate on GDP, the forecast for GDP gets worse.

The “brace-for-impact” forecast

If we assume a stronger effect of the interest rate on GDP of –1.0, the forecast gets dire:

This forecast is clearly very pessimistic.

Will it come to that? My best guess is “no.” I think the brace-for-impact forecast is least likely.

First, it is unlikely that we will see such a big drop in growth in the fourth quarter of this year. We are currently a month into the fourth quarter and thus far preliminary estimates are positive (at least, my favorite “nowcast” from the Federal Reserve Bank of Atlanta is positive).

Second, the economy appears to have “weathered” the storms of 2022 relatively well—the incessant inflation, the war in Ukraine, turbulent energy markets, and so on. Certainly those factors helped knock growth into negative numbers the first half of this year, but the economy rebounded over the third quarter. The effect of those factors may have already done their worst damage to real GDP.

Third, consumer spending is proving to be relatively stable in 2022, which makes me relatively optimistic for 2023. I discussed as much a few months back, and recent data appears to corroborate this view (I will look again at consumption data in a follow-on post).

Of course, more bad stuff can happen in 2023. But, given the information we have now, I suspect the best forecast is somewhere in between my “baseline” forecast and my “soft-landing” forecast. In that case, my plug-and-chugging suggests a slightly rosier outlook than the Fed’s forecast (which is close to my soft-landing” estimate for 2023). I will track this prediction, of course, as we slog our way towards 2023.

There is always some movement around the Fed’s specific target for the federal funds rate. For example, the rate ended the day on Thursday, November 3rd, at 3.83 percent.

I assumed values for the effect for two related reasons: 1) there is not a conclusive estimate of that effect from economic research; and 2) over the last twenty years (if not longer) the federal funds rate has not changed by large amounts very often (for a good portion of the last twenty years the rate has been close to zero). When a variable does not change very much over time, it is difficult to measure the effect of a change in that variable on another variable. This feature of the federal funds rate makes it challenging to pinpoint exactly how a change in the Fed’s key interest rate matters for the macroeconomy. Overall, the value of -0.25 is closest to recent efforts to estimate the effect of monetary policy GDP.