High’ish and Variable Inflation

Are things getting worse?

Rate-Cut-Watch 2024 continues as last week the Fed decided to once again keep their target interest rate unchanged. In their policy statement, the Federal Open Market Committee noted that “In recent months, there has been a lack of further progress toward the Committee's 2 percent inflation objective.” They also noted that the economy continues to remain relatively strong, which likely helps explain that “lack of further progress.”

One fear is that while we have gotten closer to the Fed’s 2 percent target for inflation, the recent stubbornness of the inflation rate may be a harbinger of no-rate-cuts-anytime-soon-doom, if not the source of increasing macroeconomic angst (as if we are not in a perpetual state of such angst).

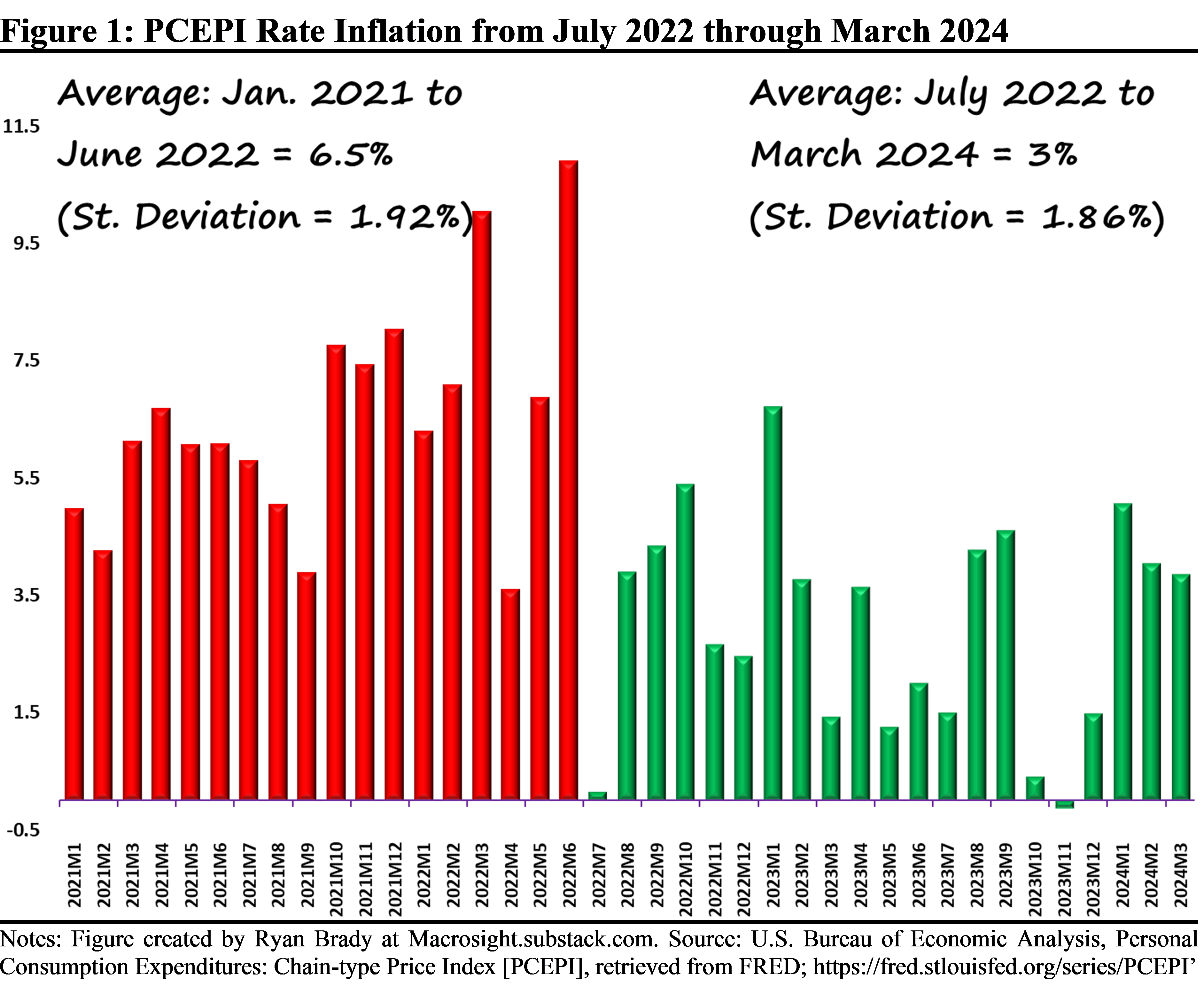

On the bright side, the rate of PCEPI inflation, the Fed’s preferred measure, has averaged an annualized rate of 3 percent per month since July of 2022 (from January 2021 to June 2022, the rate of inflation averaged 6.5 percent). However, over the first three months of 2024, the PCEPI rate has equaled 5.1 percent, 4.0 percent, and 3.9 percent, respectively (rates annualized).

Yet, while the inflation rate’s “lack of further progress” is frustrating, it is not necessarily time for panic. The data provides a reason to be optimistic. First, “ups and downs” of the rate of inflation are normal, even as disinflation is occurring. Second, the ups and downs of the past couple of years, in particular, are not abnormal, in spite of how abnormal things have seemed.

The latter, of course, may be difficult to believe, but let’s take a look at the data to see what I mean.

A storm brewing?

Figure 1 displays the PCEPI rate of inflation from January 2021 through March 2024, with an emphasis on comparing the January 2021 to June 2022 period (the end of which marked the peak of Beastflation) with the July 2022 to March 2024 time frame. The former period is emphasized in red, the latter in green.

The annotations on the figure highlight two insights: 1) The average rate of PCEPI inflation since July of 2022 (a span of 21 months) has been 3 percent versus the 6.5 percent over the preceding 18 months; and 2) The volatility of the rate of inflation across the two periods—as measured by the standard deviation—has been similar if not essentially the same.

Why is the latter noteworthy? That particular nugget of information may be helpful in understanding where inflation may be heading.

Calm(er) Waters

A piece of conventional wisdom among monetary economists and central bankers is that low rates of inflation imply stable rates of inflation, and vice versa. In such environs, too, it makes it easier for the likes of Jerome Powell & Co. to stabilize the rate of inflation around the 2 percent target.

With that in mind, Table 1 displays the average rate of inflation across different eras, along with the standard deviation in each era.

The first row of the table marks the period of history known as the Great Inflation (give or take a few months). The 1983 to 2020 period delineates the Great Moderation broadly speaking (discussed here by Macrosight)1, and the last two rows show the compare-and-contrast emphasized in Figure 1.

The key takeaway is to notice that not only has the volatility of the rate of inflation declined over time, but that volatility is actually lower since 2021 than during the Great Moderation. The latter has the word “moderation” in it for a reason—inflation was relatively stable over this era. Yet, here we find inflation has been relatively more stable recently.

I know, this is surprising and even a bit of a head-scratcher. Why that might be the case will require a lot of economic and data analysis beyond the scope of a blog such as this. Regardless of the why, this information may offer some clue as to what may be coming next for inflation (and by extension, for the potential for interest-rate-cuts).

Changing Course

When inflation is stable, the macroeconomic crystal ball is a bit less murky than in the case with high inflation volatility. That means that a variable like inflation is easier to forecast. Why? Because lower volatility may mean that a variable is more “persistent” over time, and that implies that recent history should prove a more reliable indicator of the future path of the series than otherwise.

With that in mind, Figure 2 displays Macrosight’s forecast for April 2024 (not yet reported at the time of this post) and for the following four months, along with the past 12 months of actual data for the PCEPI rate of inflation.

The Macrosight forecast suggests a drop from March to April of about 1 percent, from 3.9 to 2.9 percent, followed by a gradual descent for the series (recall these numbers are annualized).2

A drop from 3.9 to 2.9 would certainly be most welcome—no doubt met by cheers from rate-cut enthusiasts—yet that would be nothing unusual given the fluctuations you can see in Figure 2 the past 12 months (where the average rate of PCEPI inflation has been under 3 percent).

Is such a one-month-drop likely? I think that is a reasonable expectation (on a month-to-month basis—meaning not annualized—that would be a decline from 0.32 percent in March to 0.24 percent change in April). The volatility of the series has been in line, if not more tempered, with what history tells us it should be. As mentioned before, “ups and downs” are normal, even relatively big ups or big downs here and there. Looking ahead the next few months, the data gives us reasons to be optimistic that inflation is (crossing fingers) getting back to normal.

Some consider the 2008 financial crisis and the Great Recession the end of the Great Moderation. But, inflation averaged less than two percent from mid-2009 (the end of the Great Recession) to the end of 2020. It seems reasonable—to me anyway—to include that decade as part of said Moderation.

The values of this forecast are based on the history of PCEPI inflation from January of 2000 through March of 2024. Using that data, I estimated the current value of inflation as a function of the past four months’ values (see this Macrosight post for an explanation of this approach). Estimating that model provides the measure of “persistence” for inflation (how much the past months’ inflation rates are correlated with today), which then allows one to extrapolate the model over the next five months. In that extrapolation, the most recent month is the most important (meaning that month has the highest weight in the model).

I also considered other factors into the model, including a measure of inflation expectations and a measure of the output gap (as represented by the difference in the unemployment rate and the noncyclical rate of unemployment) or unemployment rate. The relevance of those variables for the inflation rate are explained in this sequence of Macrosight posts, post1, post2, and post3. However, ultimately the five-month forecast did not change substantially, though the effects of those factors were not surprising. For example, if the rate of unemployment is set higher in the model, the forecasted rate of inflation declines faster.