Time to Panic?

What a 4.3 percent unemployment rate means (and doesn’t mean)

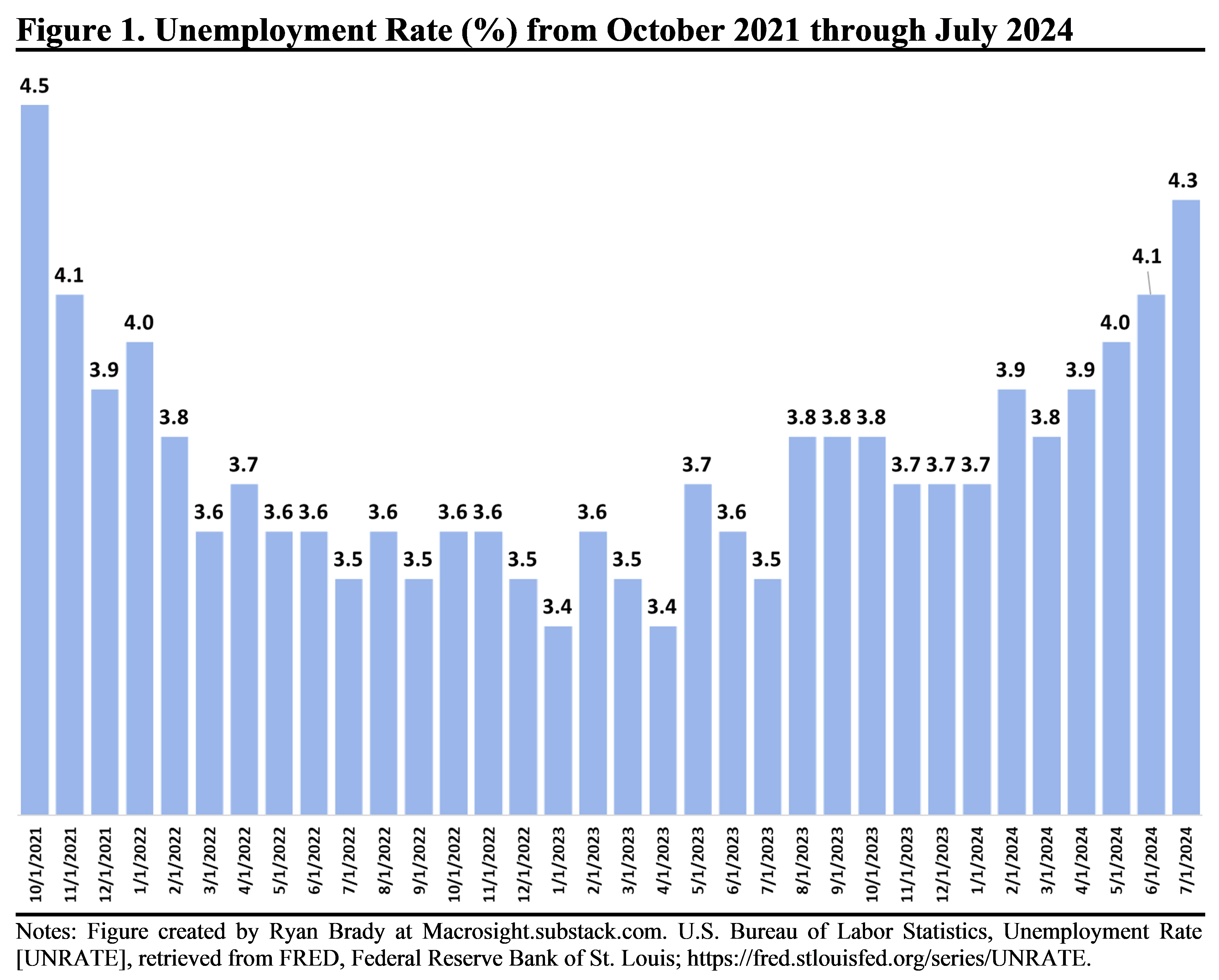

A week ago, the Bureau of Labor Statistics released the unemployment rate for July. The rate—equaling 4.3 percent—represented an unwelcome jump up from the 4.1 percent reported for June. This jump, too, not only sent the stock market into a panic but stoked fears of an impending recession.

Why the latter? July marked the fourth month in a row the unemployment rate had increased (from 3.8 in March). The value of 4.3 percent was also the highest unemployment rate since October of 2021 (when it stood at 4.5 percent).

So, is it time to panic? And, as some media outlets called for, should the Fed cut rates now instead of waiting for their next scheduled meeting in September?

My answer to both of those questions is no. I say so for at least a couple of reasons. One, 4.3 percent is still a historically very low unemployment rate; and two, it is relatively normal to get big swings in the employment/unemployment data from month-to-month—so one month need not portend our doom.

Let’s look at some data!

Reason 1: 4.3 percent is still low

An unemployment rate of 4.3 percent is still quite low by any historical comparison, and in the context of so much other macroeconomic data, does not imply a recession is on the horizon. Figure 1 displays the monthly unemployment rate since October 2021 (the last time the rate was higher than 4.3 percent).

The unemployment rate over this stretch of time represents something anomalous compared with recent history. Indeed, as discussed in this post from earlier this year, the unemployment rate has been below the natural or “non-cyclical” rate of unemployment for the better part of the past three years. That is still the case for the July rate of 4.3 percent (the current non-cyclical rate is 4.4 percent).

How about further back? Figure 2 displays the unemployment rate going back to January of 2000.

From this longer-run perspective 4.3 percent is, again, quite low. However, one can notice that the unemployment rate is persistent over time—as it increases, it tends to increase for a while; then as it falls, it does so for a while.1 Hence, it is certainly possible that as of the last few months we are looking at the beginning of an extended month-to-month increase in the unemployment rate. Is that likely?

Reason 2: July was not that unusual

Even though the unemployment rate did increase from 4.1 to 4.3 percent, there was nothing necessarily new about what happened with the labor market last month—as least not with respect to recent history.

To see that, note first that the statistic itself is simple to calculate. The BLS takes the number of people unemployed, and divides that by the labor force. The latter is the sum of two things: the number of people unemployed and the number of people employed.2

Hence, the unemployment rate will change if the number of unemployed changes, the number of employed changes, or both change at the time. In July, for example, the number of persons unemployed increased by 352,000 relative to June, yet the number employed only increased by 67,000. In the equation above, that means the jump in the number of unemployed dominated, leading to the increase in the rate from 4.1 to 4.3.

So, is 352,000 a big deal or not?

Table 1 displays the month-to-month changes both in terms of the number of persons employed and unemployed and the percentage changes of each since January 2023. (Note, numbers shown in parentheses represent a negative number, or a decline in the number employed or unemployed from month-to-month.)

The bottom row of the table shows the data mentioned above. In July of 2024, the number of persons increased by 67,000 representing a very small increase of 0.04% over the previous month. The 352,000 increase in the unemployed amounted to just over a 5 percent increase.

The table also reveals that we get quite a bit of variation in both the employed and unemployed month-to-month. In January of 2023 we had an increase of almost a million employed persons relative to the previous month. While just this past May there was a decline of employed persons by about 400,000. As such, the stock market nor anyone else should be surprised that things change a lot every month—one big increase in the employed does not signal a guarantee of sunny days ahead, nor does a substantial decline augur our doom.

Indeed, Table 1 further reveals that, aside from last month, since January of 2023 there have been four other months when the unemployed increased by 4 percent or more (I chose 4 percent somewhat arbitrarily as a cut-off for a “big” jump). Those other months had some eye-popping numbers, too. A year ago in August, for example, we saw an increase of over 400,000 counted as unemployed. Perhaps then the July 2024 number needs not be so fear-inducing.

On the other hand, a 4 percent or more increase in the number unemployed is not that common historically. Since 1990, such an increase has occurred only 31 times (out of 414 months). That implies we should see an increase like that about every 13 months, as opposed to the every 3 to 4 months it has occurred since the beginning of 2023. From this longer-run perspective, what happened with unemployment in July is unusual so maybe we should be very concerned!

What to think?

On balance, this blog still thinks the macroeconomy appears stable and will continue to remain so for the foreseeable future. In fact, for interest-rate-cut enthusiasts, the July “spike” in unemployment should solicit cheers—this makes it all the more likely that the Fed will cut the federal funds rate in their September meeting. If so, we might see an uptick in investment expenditure, consumer spending—which has been and still is stable—and expenditure related to the housing market. But, we’ll see what happens next!

The exception to that general description was the Covid-19 experience when, due to the shut-downs, the rate spiked quickly the fell quickly as things opened up. During the Great Recession the increase was dramatic and persistent, while the decline thereafter was gradual.

Macrosight provided some explanation on the unemployment rate here. Also, the BLS defines the unemployment as follows: “The unemployment rate represents the number of unemployed as a percentage of the labor force. Labor force data are restricted to people 16 years of age and older, who currently reside in 1 of the 50 states or the District of Columbia, who do not reside in institutions (e.g., penal and mental facilities, homes for the aged), and who are not on active duty in the Armed Forces.”