The Fed and the Hungry Beast

Have they slowed the American Consumer down?

Over the past two years, the Federal Reserve’s target interest rate, the federal funds rate, has increased from (essentially) zero to about 5.3 percent, where it stands today. The entire point of this persistent increase has been to bring down the rate of inflation. Why raise the interest rate to do so? Because that is how the Fed believes that monetary policy can slow the economy. Macrosight has previously explained the “whys” and “hows” of that philosophy. The Fed’s effort thus far begs the question: has it worked?

Recent inflation data suggests as much. Yet, as noted in the last Macrosight post, the Fed does not appear eager to reverse course and start lowering rates. That reluctance is likely due to fact that real GDP growth is still relatively strong, and the rate of inflation is not yet back to around 2 percent (the Fed’s target rate for inflation). So, what will it take for the ongoing disinflation to continue, enough so that the Fed lowers rates? As early readers of Macrosight might recall, this outlet has a particular affinity for the American Consumer, a.k.a, the Hungry Beast. So, let’s see what said Hungry Beast has been up to.

The Beast Awakens

Figure 1 displays the monthly growth rates of total consumption spending for the U.S. economy, and the three sub-categories of consumption—durable goods, nondurable goods and services—from 2019 through 2023. The varying colors correspond to each year, and the corresponding percentages in boxes identify the average growth rate in each year of each consumption category.

The story of consumer spending the past few years is thus: spending during the second half of 2020, and over the entirety of 2021 was explosive and historic; in 2022 the Hungry Beast slowed considerably and spending cooled; yet in 2023 the Hungry Beast came back to life.

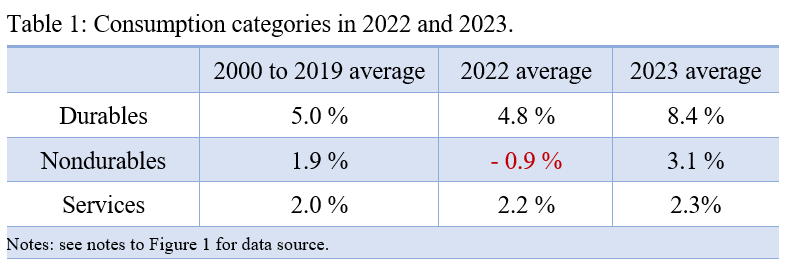

That story is generally true for each category of consumption. Macrosight has discussed consumer spending over 2020 and 2021 in detail here and here. What is pertinent to understanding what the Fed will do in 2024 is what has happened over the past two years. Table 1 emphasizes the data shown in Figure 1 for the years 2022 and 2023 (alongside the pre-2020 average).

In 2022 the Hungry Beast hit the brakes on its gluttonous romp of 2021. That is evident looking at the graphic for each category in Figure 1, and it is also evident by noticing how the 2022 percentages compare to the 2000 to 2019 averages (which Macrosight considers “normal” for the Hungry Beast). In 2022, spending on durables went back to normal, nondurables went below normal, and services were pretty close to normal.

Back to Normal

Getting back to normal or below normal in 2022 suggests at least a couple things.

It makes sense that inflation finally cooled over the second half of 2023. High rates of spending push inflation up, and slowing rates of spending help bring inflation down. Moreover, inflation likely tails, or “lags,” the changes in spending, as inflation expectations take time to adjust downwards.

It also makes sense why the rate of inflation, though dis-inflating, is still above the Federal Reserve’s 2 percent inflation target. After its 2022 hangover, in 2023 the Hungry Beast started rooting around in the dirt again, its snout once again piqued. So much so that spending on durables in 2023 jumped above its long-term average to 8.4 percent. Nondurables jumped, too, recovering from its 2022-swoon by rising to 3.1 percent, also above its long-term average. Only services kept relatively steady from 2022 to 2023 (with rates in both years just a bit above that category’s long-term average).

Back above Normal (uh-oh)

Yet, being back above normal in 2023 also suggests some things.

While it is generally a positive thing to see the American Consumer recover its appetite, the 2023 growth rates of the consumption categories imply that there is still a lot of “pressure” on inflation. Consumption spending makes up two-thirds of GDP, and changes in consumption matter greatly for changes in GDP.

While inflation did fall over the second-half of 2023, even as the Hungry Beast was getting its mojo back, the “lag” effect mentioned above with respect to inflation expectations means there is not a period-for-period correlation with inflationary pressure related to consumer spending. In that respect, the Beast’s 2023 consumption rates may be a “leading indicator” of future inflation.

Finally, the 2023 consumer spending data imply the Fed’s job is not yet done. In spite of the rate hikes over 2022 and 2023, the Hungry Beast still feasted at a healthy rate. It is possible, and even likely, that consumer spending “lags” changes in interest rates—meaning it takes awhile for changes in spending habits to adjust to higher interest rates. This is yet one more reason why the Fed is being cautious. They need to wait and see.

More to do

Of course, parsing spending behavior across time as I have done in this post offers “analysis by conjecture.” For a bit more rigor, one could use forecasting methods to assess the connection between rates and consumer spending, as Macrosight did previously here and here for GDP. In addition, one could also bring more data to bear on the issue.

For example, one could consider the relative importance of durables, nondurables and services in explaining rising (or falling) inflation by analyzing the price index related to each consumption category. That should provide some insight on how each category has mattered for explaining inflation in the past, as well as providing some insight on what to expect in 2024.

Yet, for now, this post is already long enough. Macrosight will consider some of those additional areas of analysis in future posts.

Postscript

For those that are curious, or desire a refresher, here I briefly describe the different consumption categories. As categorized by the Bureau of Economic Analysis (BEA), consumer spending includes durable goods, nondurable goods, and services.1

The gist of each category is as follows:

Durable Goods include “tangible” items that can be stored and inventoried, in addition to other things like software products. A durable good is one that a household will keep for three years or more. Examples include cars, furniture, appliances and other equipment most persons hang onto for a while.

Nondurable Goods are also “tangible” items that can be stored and inventoried but are things that a household will replace in under three years or less. Examples include clothing, shoes, food and drink purchased for consuming at home, and day-to-day products like toothpaste and deodorant.

Services are things that cannot be stored and, as such, are consumed at the time of purchase and, typically, at the location at which the service is offered. Examples include eating out at restaurants (or take-out), health care-related visits, transportation services (Uber or Lyft, e.g.), spending on recreation outside of the home, and financial services.

Of these three categories, the last one, services, makes up most of our spending, comprising approximately 65 percent of all consumption on a year-to-year basis. Nondurables make up about 20 or so percent of our spending while durables are about 15 percent (see this Macrosight post for some more details).

See Chapter 5 of the NIPA Handbook at https://www.bea.gov/resources/methodologies/nipa-handbook/pdf/chapter-05.pdf.)